Early on in my Wall Street career, I got assigned coverage of tech stocks...

As you might expect, I quickly learned that it was a lot more fun than some quieter corners of the market – like utilities.

From a career standpoint, following utilities wasn't quite a graveyard job. But it was close.

In an exciting quarter, a tech company might have 50% revenue growth. And it could have introduced a cool new product or service.

And for a utility, an exciting quarter might mean revenues were up 4%... with a $0.02 increase to the dividend.

Personally, I had nothing against utility stocks. But they felt like the financial equivalent of watching paint dry.

However, that's all different today...

The transmission and distribution of power is still regulated. But power generation is a free-market, competitive business.

And what was once a sleepy corner of the market is now a key player in the AI revolution.

The real surprise here is how the whole business is growing...

According to Bank of America Institute, U.S. demand for electricity grew by roughly 0.5% per year from 2014 to 2024. But over the next 10 years, it's expected to grow by about 2.5% annually.

That's five times the historical rate.

My younger self would have never predicted this...

Utilities are no longer boring, low-growth dividend stocks. They're now some of the market's most compelling growth opportunities.

And the question for investors isn't really the "if" around that demand. Instead, it's how to pick the winners in capturing the value it creates...

Hundreds-of-Percent Gains for Certain Utility Stocks

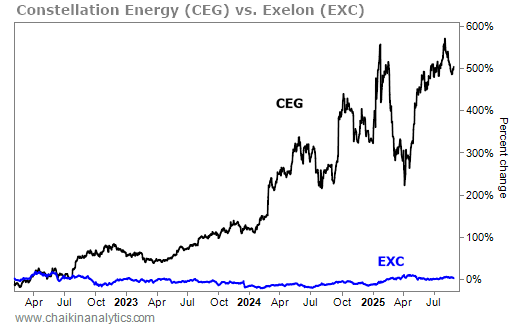

Exelon (EXC) is a great example of change within the utility industry...

At its peak, Exelon was the largest U.S. utility by revenue – serving about 10 million customers. Its subsidiary PECO Energy was even an original Thomas Edison utility incorporated in 1902.

In early 2022, Exelon split into two companies.

Its power generation assets went into a new company called Constellation Energy (CEG). And its transmission and distribution assets stayed in the "old" Exelon.

Regulation was a big driver of the split...

In 2019, the Federal Energy Regulatory Commission issued a decision that changed the rules around subsidies for "clean energy" assets.

This hit Exelon hard.

It had the largest fleet of nuclear power plants in the U.S. And at its peak, Exelon produced about 12% of the country's carbon-free energy.

Exelon also saw that power generation and transmission and distribution had become completely different businesses.

Generation was unregulated and had huge potential for growth. Transmission and distribution were still regulated and had little potential for growth.

And from an investor standpoint, separating the two was a home run...

Just take a look at the difference in stock performance since the split completion in February 2022...

That's a great example of how the market views these two kinds of businesses.

In the utility world, folks call Constellation an independent power producer ("IPP"). Constellation is one of the five largest publicly traded IPP companies in the U.S.

The other four are NextEra Energy (NEE), NRG Energy (NRG), Talen Energy (TLN), and Vistra (VST).

IPPs are the hottest part of the utility sector. That's because they're best positioned to benefit from that growth in power demand.

And they're better positioned to capture that growth – since they aren't regulated in the same way as other utilities.

IPPs can look at where demand is growing and invest for the best opportunities. Regulated utilities still have to consider their rate base before putting any money to work.

And the growth in demand isn't just related to AI...

As I mentioned earlier, U.S. demand for electricity is expected to grow by about 2.5% annually over the next 10 years.

At 1%, building electrification is the biggest driver of the increase. The other drivers are data centers at 0.5%, increased industrial consumption at 0.3%, and electric vehicles at 0.2%. (The final 0.5% comes from the historical annual growth figure.)

So even if you're not a big believer in the AI story, there are still strong tailwinds from other avenues of growth.

Last year, the IPP stocks I mentioned gained an average of about 131%. That compares with a roughly 20% increase in the Utilities Select Sector SPDR Fund (XLU). Meanwhile, the S&P 500 Index gained 23% last year.

This year, those IPP stocks are up roughly 45% on average. XLU is up roughly 11% in 2025. And the S&P 500 is up about 10%.

Talen is the highflyer in the group. It soared roughly 215% last year. And it's up about 88% in 2025.

Today, investors in utilities have a big choice...

They can invest in the growth potential of the IPPs. Or they can stay with those "steady Eddie" low-growth dividend payers.

Sometimes, the future sneaks up on you in unlikely places. The boring utilities I once passed over are now delivering incredible returns.

And covering utilities is no longer the graveyard shift. It's a fascinating corner of the market to watch.

Good investing,

Joe Austin