If you're rich, debt is a beautiful thing.

You can do a lot with it...

Debt can supercharge your investments. It creates what we call "leverage." And it allows you to earn higher returns by taking on more risk.

Debt can also help you acquire more productive assets. Just think about a manufacturer taking on debt to buy more machinery.

In the right hands, the risk of debt can be minimal. It's a tool wielded by savvy entrepreneurs.

But for consumers, it's a different story...

Consumer debt falls into just a handful of categories. But the largest is easily mortgage-related.

Auto loans, student loans, and credit cards make up most of the rest. And those tend to be a fraction of the mortgage category.

Now, you've likely heard about the possibility of a 50-year home mortgage. President Donald Trump recently proposed the idea. And it has been all over the financial media.

Folks, you need to take this seriously. It's not just a "Trump thing."

It's a part of a long-term trend that's splitting the American consumer into two categories – those that will live in debt forever, and those that won't.

Put simply, this is a rise of American "serfdom." And understanding how the system works will determine your family's future for generations...

A Concerning Trend With Auto Loans

I get it...

The claim that we're in the process of creating a class of "serfs" probably sounds far-fetched to you. After all, I picture funny, feudal-era drawings of knights and peasants when I hear the term.

But don't let that fool you. Massively long loan terms would build a working class built on indebtedness... endlessly making payments on unobtainable, expensive assets.

You don't have to take my word for it, either. The data makes it clear...

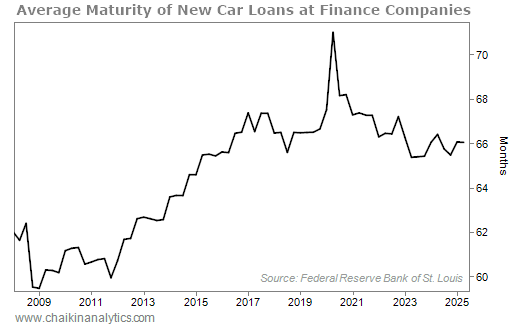

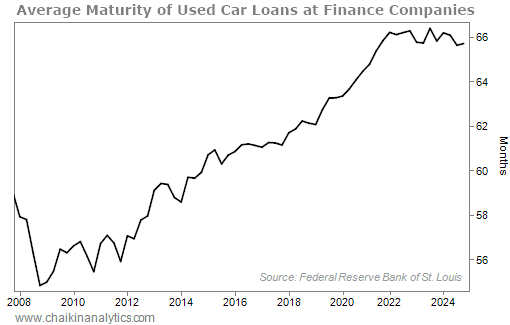

Since 2009, the term length of consumer loans has surged higher. It's easiest to see this in auto loan data.

Take a look...

As you can see, loan terms for both new and used cars have increased.

Heck, according to data from automotive-research firm Edmunds, the average term for new car loans stands at nearly 70 months.

Edmunds also says that roughly 22% of consumers opt for an 84-month auto loan. That's seven years.

According to S&P Global Mobility, the average vehicle age in the U.S. is nearly 13 years. So an 84-month loan would be more than half of the expected lifespan of a vehicle.

Beyond that, a longer loan term means that you'll pay more in interest...

Let's say you buy a $50,000 car with a $10,000 down payment and an 84-month loan at a 5% interest rate. (For the sake of simplicity, we won't factor in costs like sales tax or other fees.)

You'll pay nearly $7,500 in interest. That's about 15% of the sticker price of the car. And remember, the loan term is more than half of the average age of a car in the U.S.

It's a huge win for financial institutions. And those institutions will benefit even more if auto loan terms keep climbing.

Meanwhile, that $7,500 in our calculation is money that you're not investing. It's just going toward paying down a consumable good.

Again, these 84-month loan terms are already happening. And with a potential 50-year mortgage on the horizon, the figures get even more extreme...

A Bleak Reality for a 50-Year Mortgage

Let's say you buy a $500,000 house with a $100,000 down payment – or 20% of the house price. And you take a 50-year loan term with a 5% interest rate. (Again, we'll keep the calculation simple by not factoring in things like property taxes or insurance.)

That's about $690,000 in interest over the life of the loan.

It's a staggering figure. And it gets downright bleak when you consider that the median age of a first-time homebuyer has soared to 40 years old... while the U.S. life expectancy rate is just below 80 years old.

Folks, there's no getting around the reality of this...

Some Americans are going to make investments that grow their wealth. And others will fall into this modern-day "serfdom" of debt.

Good investing,

Vic Lederman